Malaysian palm oil exports to Sub-Saharan will experience a significant rebound in 2022 after a modest decline recorded this year, but this recovery will be asymmetrical between the region’s countries, in a context of uncertainty due to the setback emanating from the COVID-19 pandemic.

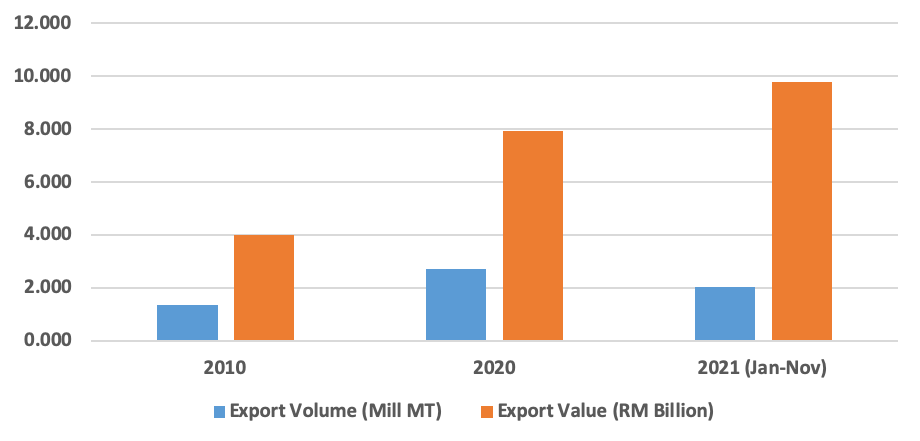

From a global perspective, as a market destination of Malaysian palm oil exports, Sub-Saharan Africa(SSA) took in about 15.5 percent of total MPO export in 2020. In comparison to 2010, when MPO exports to the region totalled just 1.335 million tonnes, the export volume has doubled after ten years to reach 2.702 million MT in 2020. In terms of value, MPO exports to SSA reached RM 7.909 billion in 2020 compared to just RM 4.004 billion in 2010. For this year, from Jan-Nov 2021, the export volume has reached 2.200 million MT with an export value of RM 9.782 billion.

Fig 1: MPO Export Performance to Sub-Saharan Africa (2010 -2021)

Source: MPOB

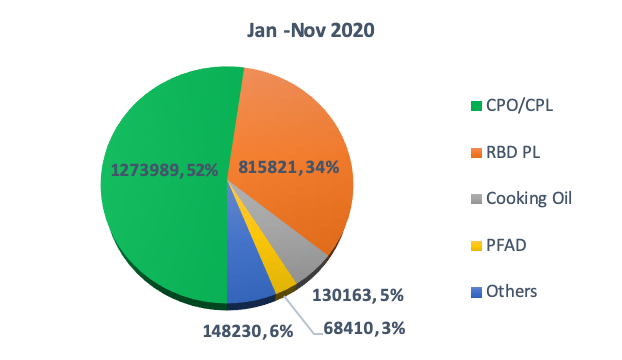

2021 MPO Export Performance (Jan-Nov)

Due to the high price of palm oil in 2021 and other challenges associated with the COVID-19 pandemic, Malaysian palm oil exports performance to the Sub-Saharan Africa region have declined modestly. Until November 2021, Malaysian palm oil exports to Sub-Saharan Africa region reached 2.2 million MT which is about 9.7 percent lower than the corresponding period last year.

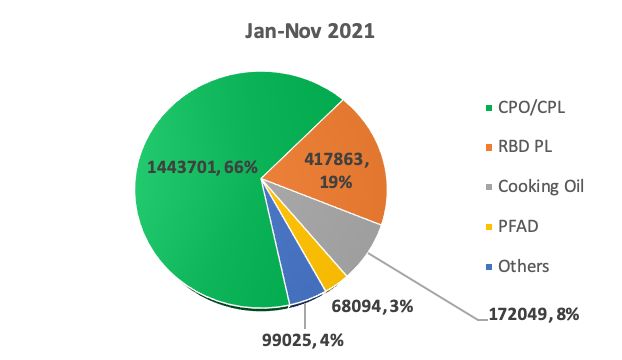

Fig 2: Breakdown of MPO Exports (MT, %) to SSA, Jan-Nov 2020 – Jan -Nov 2021

Source: MPOB

The drop in MPO exports to SSA can be attributed to higher prices of RBD palm olein in 2021 compared to last years’ prices which resulted in a 48.7% drop from 815,821 MT to 417,863 MT. The current pandemic situation has made the cost of freight even higher, therefore increasing the cost of imports. On the other hand, crude palm oil/crude palm olein (CPO/CPL) exports have increased by 13.3% to reach 1,443,701 MT. For Jan-Nov 2021, CPO/CPL contributes about 66% of total imports from SSA, up from 52% a year ago, while RBD palm olein constitutes about 19% of total import, down from 34% last year.

Table 1: Quarterly Average Prices of Malaysian RBD Palm Olein (fob) in US-$ per MT

| Year | Jan-Mar | Apr-Jun | Jul-Sep | Oct-Dec |

|---|---|---|---|---|

| 2020 | 678 | 567 | 703 | 856 |

| 2021 | 1017 | 1079 | 1133 |

Source: Oil World

Kenya Stands Alone at the Top

While most countries in the region have imported less MPO this year, Kenya is an exception. So far this year, Kenya has imported 593,097 MT of MPO which is substantially 43.90 percent higher than last year’s import volume of 412,152 MT. The strong surge in MPO imports in Kenya can be attributed to an increase in demand for CPO by the local refineries in Kenya and neighbouring Tanzania and other land-locked countries such as Uganda, Rwanda, Burundi, and the Democratic Republic of Congo.

According to the World Bank, Kenya’s economy has demonstrated resilience to the COVID-19 shock, with output in the first half of the year being better than pre-pandemic levels. In 2021 as a whole, Kenya’s gross domestic product (GDP) is expected to grow by 5%, one of the fastest recoveries among Sub-Saharan African countries.

The World Bank attributed Kenya’s economic resilience to diversified sources of growth and sound economic policies and management. Economic activity in Kenya has continued to adapt to the pandemic and associated restrictions. The vaccine rollout, which had a slow start due to supply constraints, has picked up as new shipments of vaccines have arrived, particularly since September. This has supported economic recovery and growth through the third quarter of 2021.

Performance of the Rest of the Importing Countries

Like other economies around the world, SSA was hit by the coronavirus-induced crisis, as various restrictions were imposed to fight off the pandemic, limited revenues, and reduced growth. With more than 40 countries and territories in Sub-Saharan Africa, palm oil importers in this region can be divided into three main categories. The first category is the traditional buyers of MPO that consists of the top six buyers from the region with an import volume of MPO exceeding 200,000 MT each. These countries are Kenya, Nigeria, Mozambique, Ghana, South Africa, and Tanzania. During Jan-Nov 2021 period, the six countries above imported 1.641 million MT of MPO which represents about 74.6% of total MPO imports by the Sub-Saharan Africa region.

Traditional Buyers of MPO (Annual Import Volume of more than 200,000 MT)

| Jan-Nov 2021 | Jan-Nov 2020 | Diff (Vol) | Diff (%) | |

|---|---|---|---|---|

| Kenya | 593,097 | 412,152 | 180,945 | 43.90 |

| Nigeria | 284,911 | 310,360 | (25,449) | (8.20) |

| Mozambique | 263,965 | 287,711 | (23,745) | (8.25) |

| Ghana | 215,356 | 225,552 | (10,196) | (4.52) |

| Tanzania | 162,360 | 184,867 | (22,507) | (12.17) |

| South Africa | 121,858 | 208,773 | (86,915) | (41.63) |

While most countries imports of MPO have dropped to within acceptably modest decline of less than 15 %, South Africa MPO imports reduction was at an alarming 41.6% lower than last year’s. Oil World forecasts that overall imports of South Africa oils and fats has plunged by 20% in Jan-Dec 2021 period to 739,000MT from 925,000 MT last year, as a result of rising of domestic production and sideways trend of consumption. Oil World also reported that Nigerian palm oil imports have declined by 100,000 MT so far this year, resulting in steep price increases in local market and curtailing consumption. Delays in shipping owing to container shortages have magnified the reduction of palm oil inventories in Nigeria and other West African countries, leading to exploding local prices in the course of 2021.

Re-Exporting Countries and Emerging Market

The second category of MPO importers from SSA is the re-exporting or transshipment market where these countries imported a large volume of Malaysian palm oil, with the main objective of re-routing to other destinations. These countries are Togo, Benin, and Ivory Coast which are located in the West Africa region. In 2020, these three countries imported 339,000 MT of Malaysian palm oils but most of these products ended up in the neighbouring countries such as Nigeria, Niger, Mali, Chad, or Burkina Faso. Strategic location, favourable import duty policy, and an access port to cater for other countries in the hinterland give Togo and Benin especially an advantage as a re-exporting hub or as a gateway to the West African region. However, land border closures due to the pandemic have had a deep impact on their economy, hence lower imports of Malaysian palm oil this year. Malaysian palm oil imports by Togo and Benin have dropped by 21.92 % and 63.95 % respectively. As the country’s borders remain closed, business and exports are restricted between several of their neighbours in the region, such as states like Nigeria, Ghana, Burkina Faso, Mali, and Niger.

| Jan-Nov 2021 | Jan-Nov 2020 | Diff (Vol) | Diff (%) | |

|---|---|---|---|---|

| Togo | 126,008 | 161,386 | (35,378) | (21.92) |

| Benin | 38,629 | 107,158 | (68,529) | (63.95) |

| Ivory Coast | 38,469 | 48,596 | (10,127) | (20.84) |

The third group of importers from SSA can be categorized as emerging markets that consist of 9 countries with an import volume of Malaysian palm oil ranging from slightly below 20,000 MT up to 150,000 MT per annum. Total import volumes of MPO by these countries almost reached half a million MT last year, or about 18% of the total import volume of the SSA region. However, until November this year, the import volume of MPO by these countries are only 356,000 MT or 21.2 % lower than last year’s imports.

Other Contributing Factors

Competition from other palm oil exporting countries and locally produced palm oil also contribute to the lowering imports of Malaysian palm oil by the countries in the region. For example, Oil World reported that for Jan-Sep 2021 period, Ivory Coast’s palm oil exports to the neighbouring West African countries has increased to 212,000 MT from 152,000 MT recorded in Jan-Sep 2020.

What to look forward to in 2022

Malaysian palm oil exports to the region are expected to bounce strongly in 2022 led by strong momentum created by the surge in imports by Kenya since 2020. Kenya, being the largest buyer of MPO in the region imported 520,000 MT in 2020, and so far has surpassed 593,000 MT this year, and the trend is expected to be sustained in 2022. Following a pandemic-induced economic contraction of 0.3 per cent in 2020, Kenya is expected to record a growth rate of 4.7 per cent in 2022.

While it is difficult to predict the exact quantum of growth in MPO export achievable next year, few indicators can be used to forecast the extent of recovery. The performance of countries will be based on indicators such as economic recovery, vaccination rate, population growth, spending power, and others.

If Indonesia further restricts CPO exports to force the development of its downstream palm oil industry, it will open more room for Malaysian CPO exporters to ship more CPO to Africa. CPO/CPL exports to SSA next year may increase by 15% to reach 1.65 million MT with the bulk of the shipment will end up in Kenya, Nigeria, Ghana, Mozambique and Madagascar.

Informal cross border trade is quite tough to quantify but as indicated by past MPO imports data by Togo and Benin, the volume of palm oil transshipped by these two countries to their neighbouring West African countries were quite substantial. Togo and Benin used to import in excess of 400,000 MT of MPO about 5 years ago but the volume has declined sharply since and the pandemic induced border closing has lowered the volume further. The African Continental Free Trade Area (AfCFTA) has given a new opportunity for the continent and revived hopes for recovery through trade and deeper integration in a post COVID-19 world.

Emerging countries such Madagascar, Angola and the Congo Democratic Republic have great potentials to accrue more MPO as a better economic condition will propel growing domestic demand and growth in the food processing industry

However, there are several factors creating uncertainty for global palm oil trade: an uneven pace of vaccination, emergence of the new virus variants, inflationary pressures, restrictive trade policies adopted by importing countries, disruptions in supply chains; and increased freight costs. While issues and challenges will remain, there is bound to be plenty of space and room for an increase in imports and consumption of Malaysian palm oil in this vast region with a huge population.

Prepared by Iskahar Nordin

*Disclaimer: This document has been prepared based on information from sources believed to be reliable but we do not make any representations as to its accuracy. This document is for information only and opinion expressed may be subject to change without notice and we will not accept any responsibility and shall not be held responsible for any loss or damage arising from or in respect of any use or misuse or reliance on the contents. We reserve our right to delete or edit any information on this site at any time at our absolute discretion without giving any prior notice.